Looking beyond stocks and fixed income - why private markets

Are you putting artificial limits on your portfolio?

Easily find, compare, and invest in exclusive private credit deals. Diversify and grow your portfolio with inflation- and recession-resilient short-term assets offering a range of high yields.

Since 2018, thousands of accredited investors have trusted Percent as their source for private credit investing.

Sign Up For Free

18.13%

Current Weighted

18.13%

Current Weighted

Private credit is an alternative asset class that can offer higher yield, shorter duration investments largely uncorrelated to the stock market. That’s why institutional investors are flocking to private credit and the $7 trillion private capital market.

Now, Percent gives accredited investors these opportunities too.

Learn More About Private Credit| Percent Private Credit* | Commercial Real Estate | Stock Market | Farmland | Collectibles & Art | High Yield Bonds | |

|---|---|---|---|---|---|---|

| Lower Volatility | ||||||

| Diversification | ||||||

| Investment Horizon | As little as 3 months | Years | Varies | Years | Varies | Varies |

| Surveillance & Data Availability |

Scroll to see comparison

* Percent asset-based notes

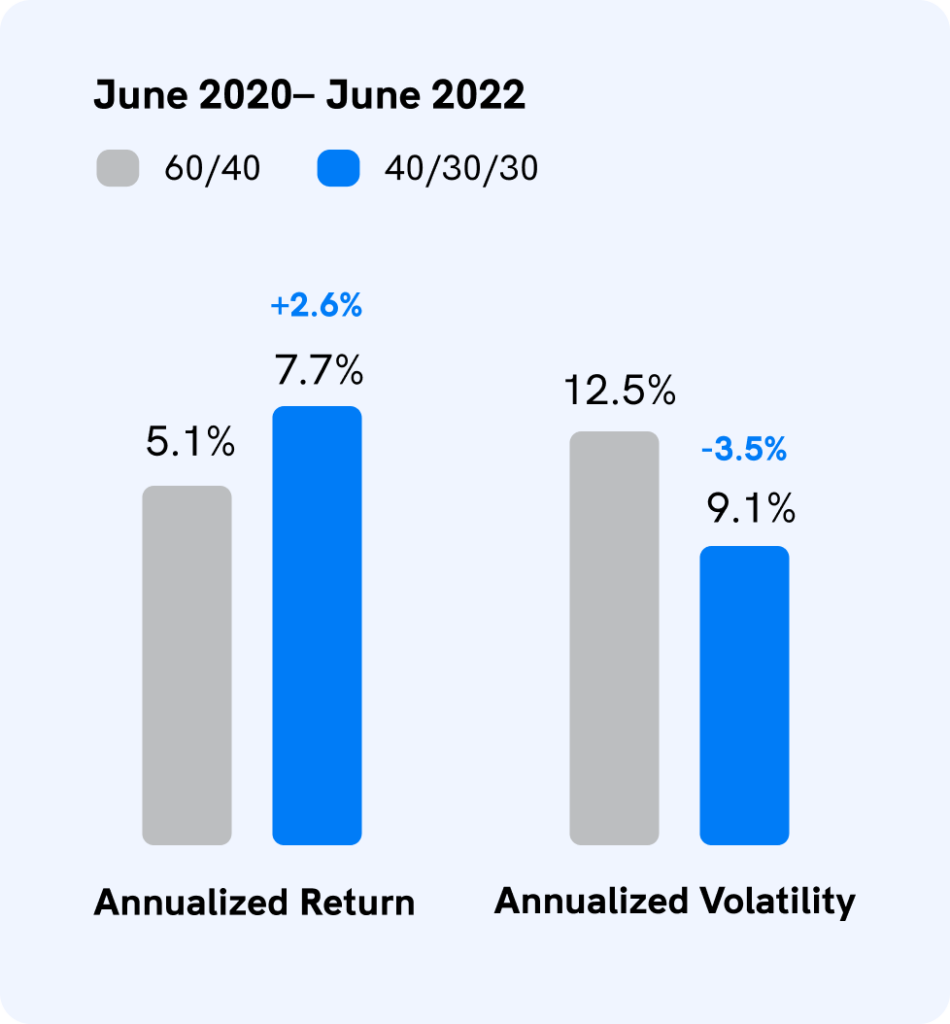

Industry research shows better returns from a 40/30/30 portfolio, with 30% allocated to alternatives like private credit.

Over a two year period, more diversified portfolios showed a 2.6% higher return rate than the traditional 60/40 equity/fixed income mix, with overall volatility lowered by more than 3%.

Like every investment, private credit involves risk. Percent encourages investors to understand their risk appetite and conduct due diligence before investing.

Diversify Your Portfolio

Are you putting artificial limits on your portfolio?

Percent’s innovative marketplace connects investors with corporate borrowers, simplifying investment and portfolio management.

Earn as much as 20% APY or more with investments that can mature in as little as one month or as long as a few years. With shorter-duration investments, you can redeploy your capital in a rising-rate environment.

Specify your desired yield and minimum investment amount during syndication. Only invest if your parameters are met. Low fees apply only to interest.

Gain exposure to different asset classes and geographies with individual deals, or use Blended Notes to quickly achieve broad diversification.

With our proprietary technology, see and compare available deals upfront. Access comprehensive borrower, deal, and market data. Then, track performance and use surveillance reports to keep informed at every step.

Receive steady cash flow – often monthly – as well as yield. Percent investments generate passive income throughout the lifetime of the deal.

Our knowledgeable Investor Relations team is available to answer your questions – just call or email us. Investors tell us that our white glove service sets Percent apart from other online investment platforms.

Get up to $500 in your Percent account after your first investment.

Private credit transactions include debt financing and privately negotiated loans.

Borrowers include small businesses and startups without access to the public markets. Private transactions finance their operations and growth and are often backed by assets, loan portfolios, or corporate debt.

Learn MoreHigher rates from borrowers who need liquidity.

Large institutional investors and financial advisors are increasing their allocations to alternatives.

Asset-based deals can offer predictable, stable income.

Low correlation and strong historical track record.

Get exclusive access to private credit investments the Percent way.